BangladeshŌĆÖs banking sector stands at the edge of a financial abyss. The latest report from Bangladesh Bank reveals a devastating truth: just 10 banks are now responsible for Tk 3.31 trillion (Tk 331,310 crore) in defaulted loans, accounting for more than 71 percent of the countryŌĆÖs total non-performing loans (NPLs). At the end of March 2025, total NPLs in the banking sector had reached an unprecedented Tk 4.20 trillion (Tk 420,335 crore), equivalent to 24.13 percent of total loans.

The alarming surge in defaults is not merely a statistical concern-it is a systemic threat. Analysts warn that the unchecked rise of NPLs, driven by decades of political patronage, poor governance, and a deeply entrenched culture of non-repayment, has crippled the banking system. What was once whispered about as bad banking practices has now emerged as a full-blown economic crisis.

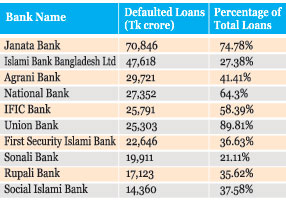

The Big Ten: Banks at the Heart of the Crisis: Among the 61 scheduled banks operating in Bangladesh, the following ten banks are bearing the lionŌĆÖs share of the burden:

Together, these institutions are choking the system with defaults amounting to Tk 3.31 trillion, a figure that dwarfs the national development budget for many years.

Janata Bank: A State-Owned Debacle: Janata Bank, one of the countryŌĆÖs largest state-owned banks, sits atop the mountain of defaults. With 74.78 percent of its disbursed loans turning bad, the bank has a staggering Tk 70,846 crore in defaulted loans. The major culprits behind JanataŌĆÖs downfall are well-known business groups including Beximco Group, which alone owes about Tk 24,000 crore, and S. Alam Group, with an additional Tk 10,000 crore in defaults.

Also included in JanataŌĆÖs infamous client list are Bismillah Group, Crescent Group, and Antex Group-all previously accused of large-scale financial fraud and capital flight. Bank insiders and analysts confirm that many of these loans were politically sanctioned with inadequate scrutiny or collateral.

Mujibur Rahman, Managing Director of Janata Bank, admitted, ŌĆ£These loans were sanctioned years ago under different managements. WeŌĆÖre currently pursuing legal avenues and recovery through mortgaged asset sales.ŌĆØ However, progress remains painfully slow.

Islami Bank: Corporate Capture and Ghost Companies: Islami Bank Bangladesh Limited (IBBL), once a model of Islamic banking in South Asia, now ranks second in terms of defaulted loans, with Tk 47,618 crore defaulted. Since S Alam Group took control of the bank in 2017, there have been continuous allegations of misuse and fraudulent lending.

Investigative reports and internal audits revealed that large sums were funneled out through ŌĆśpaper companiesŌĆÖ-nonexistent firms used to fabricate loans and siphon funds. The true scale of this corporate capture may still be underreported.A senior Bangladesh Bank official remarked, ŌĆ£This is a case of systematic abuse of a financial institution. ItŌĆÖs no longer about mismanagement-itŌĆÖs about engineered looting.ŌĆØ

Other Banks in Free Fall: Agrani Bank and National Bank round out the top four defaulters, with default rates of 41.41% and 64.3%, respectively. IFIC Bank, another private commercial bank, has also seen nearly 60% of its loans defaulted.

Union Bank, a relatively new entrant, is now infamous for having 89.81% of its loans classified as non-performing-essentially rendering it insolvent in practical terms.

First Security Islami Bank, Sonali Bank, Rupali Bank, and Social Islami Bank are all suffering from dangerously high default ratios, further illustrating the scale of rot in both state-owned and private sectors.

A Rot Beyond Numbers: Political Influence and Regulatory Capture: Economists and banking analysts say that political influence-particularly during the previous Awami League governments-played a decisive role in facilitating this crisis. Well-connected business groups secured enormous loans without proper due diligence. In many cases, loans were extended without even basic background checks or risk assessments.

During this time, loans were regularly rescheduled to avoid classifying borrowers as defaulters, and many banks used technical tricks to hide their real NPLs. Now, as the new international reporting standards are being implemented, the true extent of the problem is being laid bare.

Revealing the Hidden Defaulters: IFRS and Basel III Standards: Bangladesh Bank has recently adopted the International Financial Reporting Standards (IFRS) and Basel III guidelines for identifying NPLs. As a result, the earlier system-where interest payment alone was enough to keep a loan ŌĆ£regularŌĆØ-was abolished in August 2024.

Now, full repayment of the principal is required, and the result is stark: the curtain has been lifted on thousands of ŌĆ£hidden defaulters,ŌĆØ exposing the fragility of the system.

One central banker stated, ŌĆ£WeŌĆÖve reached the point where fiction no longer helps. The NPL figures now show the actual health of the sector-and itŌĆÖs alarming.ŌĆØ

The True Disaster: Banks Turned into Shells: Even more worrying is that some banks are now practically non-functional. A few examples:National Bank of Pakistan: 98.96% of its total loans are now defaulted.ICB Islamic Bank: 91% of loans defaulted.Padma Bank: 87.18%, still reeling from the scandal involving former ministers.Basic Bank: 69.34%, long plagued by fraud.Bangladesh Commerce Bank: 67% of its loans have gone bad.Global Islami Bank: 54.36% defaults.

These banks are being called ŌĆ£institutions dying inside the shell of a bank.ŌĆØ With defaulted loans exceeding their total capital, most are dependent on Bangladesh BankŌĆÖs emergency support or government recapitalization, putting strain on the national budget.

The Decade of Disaster: A Twenty-Fold Increase: The numbers reveal how steep the decline has been:2009: Tk 22,481 crore in NPLs.2025: Tk 420,335 crore.ThatŌĆÖs a nearly twenty-fold increase in 16 years, a growth driven largely by regulatory failure, political interference, and institutional impunity.

The Ripple Effect: Economic, Social, and Global Consequences: The fallout from this crisis is being felt across the economy:Liquidity Shortage: With trillions locked in bad loans, banks are unable to provide new credit to businesses.Investor Panic: Confidence in the banking system is rapidly eroding, with many depositors turning to gold and foreign currency.Fiscal Burden: State-owned banks are increasingly reliant on government bailouts, draining resources from development projects.Global Perception: BangladeshŌĆÖs international credit rating and reputation are at risk, making foreign borrowing more expensive.

The Need for Political Will and Systemic Reform: Experts say the road to recovery requires more than cosmetic reforms. Among their recommendations:Strict enforcement of loan classification and recovery laws.An independent Banking Commission to audit and regulate bank activities.End to political appointments in bank boards and regulatory bodies.Transparency in loan disbursement and a central defaulter database.Without bold action, the banking sector risks becoming a black hole sucking in public resources, investor confidence, and economic potential.As one economist aptly put it: ŌĆ£What we are seeing now is not just a banking crisis-it is a crisis of governance, accountability, and trust.ŌĆØ